As Canadians continue to build their lives and businesses for a digital economy that moves quickly (and around the clock), financial institutions and fintechs are under growing pressure to facilitate adaptation with tools that can match the pace and convenience of the global digital economy.

If you’re familiar with Interac e-Transfer primarily as a peer-to-peer money transfer service, you may be surprised to learn it can also help organizations reshape their payment experiences, improve their cash flow and leave behind the inefficiencies of old, slow payment methods. Interac e-Transfer for Business is the same payment platform Canadians used to send money 1.6 billion times in a single year — but scaled for businesses looking to level up their payment infrastructure to move money at the speed needed to run their business in the 21st century.

One way businesses can modernize operations is by partnering with a payment enabler that uses Interac e-Transfer to bring payments modernization within reach.

Take Paybilt, a Toronto-based fintech that helps organizations embed payment capabilities into workflows that fit their needs. Paybilt enables its customers to manage the full flow of money in and out of their businesses — receivables and payables, across any payment type. It happens through a single, fully customizable platform that adapts to each merchant’s needs, underpinned by the functionality of Interac e-Transfer for Business.

“It addresses the demand for real-time, reliable, and automated payments — across a broad range of use cases in industries including payroll, insurance, government and retail,” said Dale Sandhu, co-founder Chief Partnerships Officer for Paybilt.

Randy Sandler, Senior Product Lead of Interac e-Transfer for Business, spoke with Sandhu about what’s changing in business payments, how payment enablers help organizations keep up, and how leveraging Interac e-Transfer for Business makes it possible to modernize payment experiences.

Here are some of the highlights of their conversation.

The evolving Canadian payments landscape

Randy Sandler: Dale, you’ve spent years watching how money moves in this country — and how it compares to what’s happening globally. Let’s start with the 30,000-foot view. What’s your read on what’s changing in business payments? And where do you see the biggest opportunities for modernization?

Dale Sandhu: Canada has a highly consolidated banking system. One real upside of that is most people have access to Interac e-Transfer — a near-real-time method almost every Canadian can already use, because they’re set up for it through their bank. We saw the value in that early.

Customers prefer Interac e-Transfer: Sixty-six per cent of Canadians use it monthly and 72 per cent prefer it over other peer-to-peer payment methods.1

Randy: The question is why that value hasn’t been leveraged more fully at the business level. Businesses don’t operate on a nine-to-five schedule, and their payment infrastructure shouldn’t either. When funds are delayed, cash flow, customer experience and operations all feel the impact. That’s the gap Interac e-Transfer for Business was built to help address.

Dale: You’re right. A big part of it is education. We’re not asking a business to change the processes it’s used to. From our experience, Interac e-Transfer for Business has significant potential at the business level, but many organizations need help understanding how to make it work within their existing processes to unlock its potential. That’s where Paybilt comes in. We situnderneath them and automate the manual work — the tracking, reconciliation and the movement of money in and out, so Interac e-Transfer for Business can be used seamlessly for both receivables and payables. It gives businesses a familiar, trusted payment method with the operational ease of a plug-and-play solution.

For Paybilt, integrating Interac e-Transfer as a payment option for clients has helped our business to grow into new market segments, attract new customers and achieve promising growth.

How one platform solves a multitude of needs

Randy: That potential preference for account-based payments is something we’ve always believed merchants should be building around, not ignoring. At Interac our role is to provide the underlying capability, and partners like Paybilt help turn that into practical solutions merchants can use in real workflows. What have you built, and how does it differ from other options in the market?

Dale: Paybilt is a modular payment layer that sits between merchants and their payment infrastructure. With the addition of Interac e-Transfer, we are able to stand out with new customers looking for a real-time payment solution where speed to funds is paramount.

Randy: The payment enabler model is central to how the Interac e-Transfer for Business solution can serve the marketplace. Once a company like Paybilt integrates it, they can offer it across their entire merchant base — each with different needs, different industries, different back-office setups. It multiplies the reach significantly.

Dale: The breadth of what we’ve been able to do reflects exactly that. We’re active in insurance, government, retail, payroll and logistics. And the use cases aren’t limited to collecting money — disbursements matter just as much. A restaurant chain can pay out employee tips at the end of a shift; a logistics company can settle vendor payments in real time. And because so much of it can run over Interac e-Transfer, the money moves in near-real time on rails everyone already trusts.

Why Interac e-Transfer for Business?

Randy: What was it about Interac e-Transfer for Business that made it attractive for your customers?

Dale: Merchants kept asking for a way to enable Interac e-Transfer within their existing commercial flows as a fully integrated payment channel, with the same reliability and automation that they’d expect from any other method. And once we started building toward that, the specific features of Interac e-Transfer really stood out. The most important one: There are no declined transactions when the funds are in the account. This is a push payment. The customer logs into their own financial institution and authorizes the transfer themselves. That fundamentally changes the risk profile of the transaction.

Randy: This is one of the most consequential differences between Interac e-Transfer for Business and legacy payment methods. With pre-authorized debit — the standard EFT approach — you’re pulling from someone’s account. If the funds aren’t there, you’ve triggered an NSF situation: fees, administration, potential delays. With Interac e-Transfer for Business, the payment only happens if the money exists in the account and the account holder actively initiates it. You avoid some of the potential administrative problems.

Dale: And there’s the chargeback issue, which represents a serious cost and risk factor for certain industries — retail and hospitality especially. With Interac e-Transfer, that whole category of chargebacks and disputes goes away.

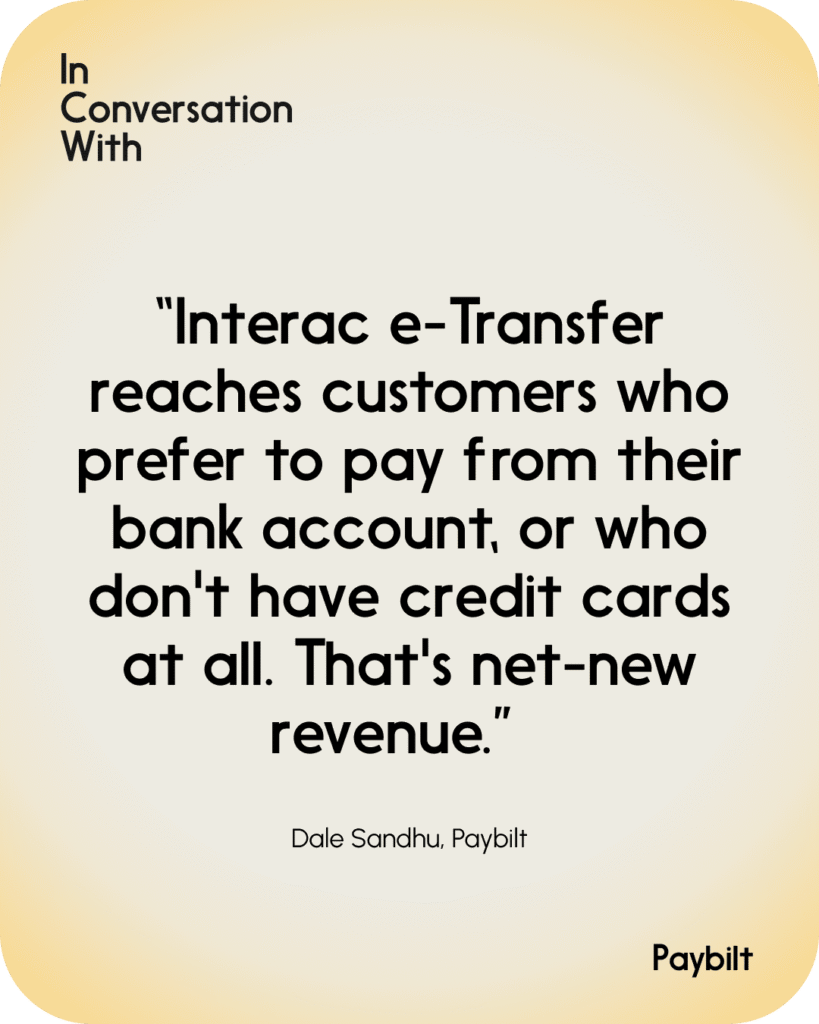

And the overall economics can work in the merchant’s favour. Early on, there was a concern that offering Interac e-Transfer might cannibalize credit card revenue. Our data tells the opposite story. We’ve seen no reduction in credit card transactions among merchants who’ve added Interac e-Transfer. It’s genuinely additive: It reaches customers who prefer to pay from their bank.

In our experience, some would rather push a payment themselves than hand over card details, and others prefer to use the money they already have rather than credit. And a lot of it comes down to trust. Interac is a brand Canadians already know as a safe way to move money, so reaching for it feels natural.

Here’s what that means for everyone in the chain: The merchant captures revenue it was leaving on the table, the customer pays the way they want, and the institutions behind Interac see more activity on rails they already own.

The pie gets bigger, and no one gives anything up. That’s net-new revenue,

Supporting automation and integration with ERP

Randy: At Interac we’ve been on a mission to help Canadian companies modernize their business payments. Interac e-Transfer for Business exists, in large part, to replace the cheque and even the EFT in a lot of cases. But how does it work in practice? Let’s talk about how solutions like yours can help companies modernize their back-office operations.

Dale: That mission — replacing the cheque and even the EFT — is exactly what we’re built to support, and in practice it’s pretty seamless. Paybilt is completely payment agnostic. We tell clients they can “BYOP” — bring your own payment. And bring your own bank. All the money movement can be unified into a single, unified stream. And then that structure of data from payments can be plugged into an API directly or set directly to your ERP systems.

Randy: The visibility piece is worth emphasizing too. One of the consistent frustrations with legacy payment methods — cheques especially, but EFT as well — is that you don’t really know what’s happened to the money. Cheques can take a long time to get to someone, they’re expensive, and when there’s a postal strike they can be delayed. With Interac e-Transfer for Business, you get real-time status confirmation. Clear success and failure signals. Plus it includes rich data; it’s ISO 20022 compliant, to help with reconciliation.

Fast payments when it really matters

Randy: Let’s talk about payments that flow back to the consumer. I know you’ve had strong uptake among the insurance industry. What can you tell me about what you’re enabling them to do?

Dale: Insurance is one of our most compelling use cases. Under the old model, if you’re owed money for a car accident, you might wait four weeks [for your insurance payout]. You might wait two months while being told the cheque is in the mail — a cheque that could easily get lost or delayed indefinitely. With Interac e-Transfer for Business, settlement is immediate the moment a claim is approved. The funds arrive in real time. This translates into enhanced customer service and satisfaction.

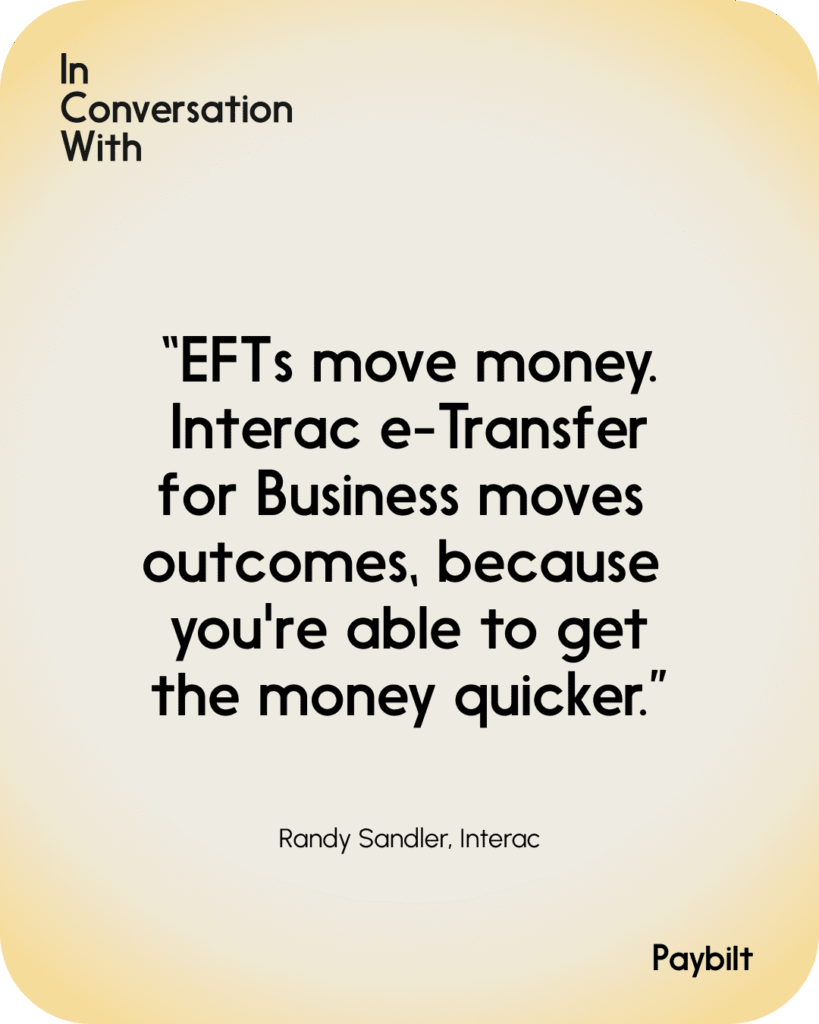

Randy: Imagine being able to pay the mechanic that’s going to fix the car right away. A lot of the time, they won’t start fixing it until they have the money. From their perspective, having the money right away could also mean savings in car rental costs. EFTs move money. I believe Interac e-Transfer for Business moves outcomes, because you’re able to get the money quicker.

New solutions for the charity sector

Randy: I understand you’ve had success making inroads in the charity sector. What has been the payment friction there and how have you had an impact?

Dale: We say to charities, “How can we help solve some problems?” And the initial problem was, “Can we bring more exposure to that subset of communities that don’t have access to a credit card to increase your donations?” What surprised us was the scale of the impact [of enabling Interac e-Transfer for donations]. One organization we work with found that payment by Interac e-Transfer made up 35 per cent of their total donations. We were expecting five or 10 per cent. And critically, those were largely net-new donors — not a shift away from other methods.

Randy: How does that work in practice? How simple is this to implement?

Dale: At an event or gala, instead of renting physical terminals, managing backups, printing receipts — all of that cost and complexity — we put a small card on each table with a QR code. Donors scan it, go through two or three clicks, and the donation is complete. And as soon as the customer makes a donation via Interac e-Transfer, they also immediately receive a receipt, which auto-reconciles for the charitable [organization].

On the back end, it can indirectly translate into cost savings for the [charities] by avoiding having finance teams manually reconcile.

For both sides, the experience is seamless. And honestly, the barrier to entry for donors couldn’t be lower. You probably have your phone on you before your wallet. You might forget your wallet — but you won’t forget your phone.

Randy: I’d say that’s all a pretty compelling case for modernizing.

See what Interac e-Transfer for Business can do for your organization

- Payments Canada: Canadian Payments Methods and Trends Report 2025 ↩︎